(ATF) The latest economic data released in China has confirmed that the country’s recovery continued in the third quarter, suggesting greater confidence among consumers and business despite caution about the impact of the coronavirus.

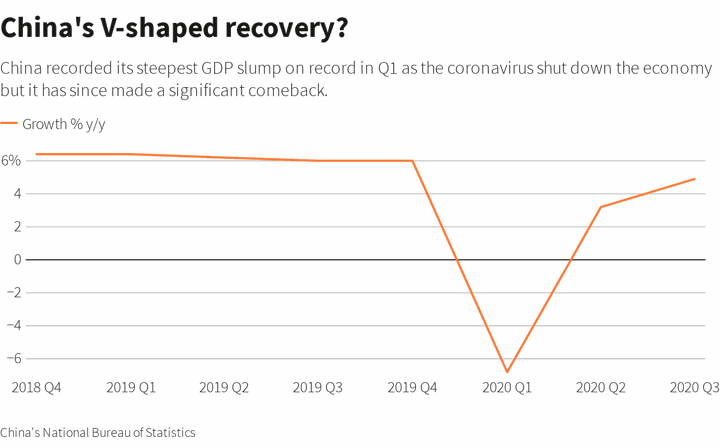

GDP growth from July to September came in at 4.9% year-on-year, which was up from 3.2% in the second quarter. The activity data pointed to stronger-than-expected retail sales and industrial production.

Ting Lu, chief China economist for Nomura in Hong Kong, said: “China’s quick recovery was a product of its stringent lockdowns, massive testing, population tracking, a large economy that can afford to be somewhat insulated, and fiscal stimulus via credit expansion.

“Strong export growth, a further recovery from the pandemic, the lagged impact of fiscal stimulus and credit growth and pent-up demand following the summer floods all contributed to the robust activity data in September. We expect a further, albeit gradual, recovery of the services sector, a steady improvement in retail sales and elevated FAI growth, especially as it relates to infrastructure.”

However, headwinds remained, Lu said, because China was not free from the risk of further waves of COVID-19, noting that pent-up demand is likely lose some steam, while medical product exports may have peaked, and Beijing is determined to cool down property markets. Plus, some social distancing measures are likely to extend into the second half “and rising US-China tensions could dent China’s exports and manufacturing investment”.

But, Nomura maintained its real GDP growth forecast of 5.7% y-o-y for Q4.

Growth more balanced

For HSBC’s Jingyang Chen, expenditure data showed that “growth has become more balanced in Q3. Consumption saw a big improvement, with its contribution to GDP turning positive to 1.7ppt in Q3 from -2.3ppt in the previous quarters.

“Net exports’ contribution to GDP growth remained largely stable at 0.6ppt. While export growth has improved substantially to 8.8% y-o-y in Q3 from 0.2% in Q2, the much stronger-than-expected pickup in imports in September (13.2% y-o-y) on the back of a recovery in domestic demand and RMB appreciation has narrowed the net export growth.”

Chaoping Zhu, a strategist JP Morgan Asset Management, said industrial sectors were stronger, while service sectors, which lagged in the previous quarters due to partial lockdowns, were catching up when most social-distancing measures were eased or removed.

Investment in private fixed assets improved significantly, while, growth rates of retail sales (consumption) and industrial production were much stronger in September than market expectation, Chaoping Chu said, adding that state-led infrastructure investment remained an important supporting factor.

Covid risk remains

China is not out of the woods yet, according to Yoshikiyo Shimamine, chief economist at Dai-ichi Life Research Institute in Tokyo, who said: “China’s economy remains on the recovery path, driven by a rebound in exports. Consumer spending is also headed in the right direction, but we cannot say it has completely shaken off the drag caused by the coronavirus.

“There is a risk that the return of lockdowns in Europe and another wave of infections in the United States will hurt consumer spending and trigger more job losses, which would be a negative for China’s economy.”

The weaker-than-expected headline figures weighed on China’s yuan and mainland stock benchmarks and capped broader market gains in Asia.

The world’s second-largest economy grew 0.7% in the first nine months from a year earlier, the National Bureau of Statistics (NBS) said.

Analysts noted that policymakers globally were pinning hope on a robust recovery in China to help restart demand as economies struggle with heavy lockdowns and a second wave of coronavirus infections.

China has only partly emerged from the record slump caused by coronavirus shutdowns in the first months of the year.

NBS spokeswoman Liu Aihua also said that growth remained patchy. “Internally, the economy is still in the process of recovery,” she told a briefing in Beijing. “Some or most of the indicators have not returned to the normal growth level, and some of the cumulative growth rate has also declined.”

But analysts were encouraged by a broader upturn in consumption and continued factory strength.

Retail sales grew 3.3% in September from a year earlier, speeding up from a modest 0.5% rise in August and posting the fastest growth since December 2019. Industrial output grew 6.9% after a 5.6% rise in August, showing the factory sector’s recovery was gaining momentum.

In the property sector, investment rose 12% in September from a year earlier, the fastest pace in nearly 1-1/2 years, providing a key support for broader investment.

The government has rolled out a raft of measures including more fiscal spending, tax relief and cuts in lending rates and banks’ reserve requirements to revive the coronavirus-hit economy and support employment.

While the central bank stepped up policy support after widespread travel restrictions choked economic activity, it has more recently held off on further easing.

The International Monetary Fund has forecast an expansion of 1.9% for China for 2020, which is close to the central bank’s own projection of 2%. That would make China the only major economy expected to report growth in 2020, albeit at the slowest annual pace since 1976, the final year of Mao Zedong’s Cultural Revolution.

Consumers step up

China’s retail spending has lagged the comeback in factory activity this year as heavy job losses and persistent worries about infections kept consumers at home, even as restrictions lifted. However, recent indicators suggest consumer activity is now turning around.

In the travel sector, domestic passenger flights in September beat their Covid-19 levels, a sign that that segment of the market is approaching a full recovery, even as international borders remain largely shut.

Auto sales marked a sixth straight month of gains in September while Ford Motor’s China vehicle sales jumped 25% in the third quarter from a year earlier.

The coronavirus outbreak, which caused China’s first contraction since at least 1992 in the first quarter, is now largely under control in the country, although there has been a small resurgence of cases in the eastern province of Shandong.

“The single most important thing for the Chinese economy in the coming months is whether service consumption can catch up,” said Larry Hu, head of China economics at Macquarie Capital in Hong Kong.

Ting Lu predicted that the PBoC would have to inject more liquidity to stem the rise of funding costs, even after 300 billion yuan in net liquidity injection via the medium-term lending facility (MLF) for October, given 10-year CGB yields have surged to above 3.2% pa in recent weeks.

“Amid heightened external challenges, Beijing’s new master plan that focuses more on ‘internal circulation’ – featuring both import substitution (or self-sufficiency) and domestic demand expansion – is becoming increasingly evident.”

With reporting and graph by Reuters.