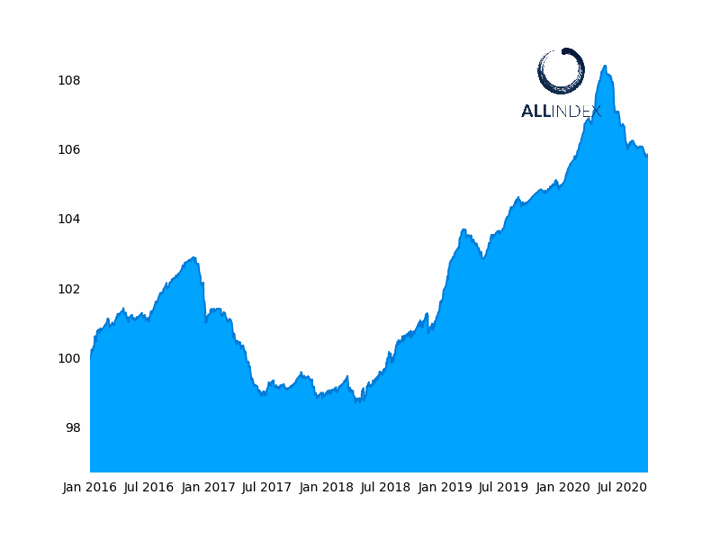

(ATF) The ATF indexes rose ahead of the monthly Loan Prime Rate (LPR) fixing due to take place on Monday, which will be a key focus for bond markets next week. The LPR is expected to remain unchanged, at 3.85% for the one-year and 4.65% for the over five-year, underscoring China’s continued economic recovery and ongoing investor confidence in China’s equity and bond markets.

The benchmark China Bond 50 index climbed 0.03% Friday, while the ATF ALLINDEX Corporates, Enterprise and Local Governments rose 0.01%. Only the ATF ALLINDEX Financial dropped, retreating 0.08% on the back of a coupon payment.

The LPR fixing comes on the heels of the People’s Bank of China open market operation on Tuesday when it injected 600 billion yuan ($88.5bn) into the banking system via its one-year medium term lending security (MLF) at the unchanged rate of 2.95%.

As 200 billion yuan (29.5bn) of MLF matured on September 17, the operation amounted to a net injection of 400bn yuan.

The ATF CB50 rose 0.03%.

The size of the liquidity injection was a surprise to markets and amounted to a 25 basis point reserve ratio requirement (RRR) cut.

“Last week the PBoC injected a large amount of MLF, more than the maturing amount, but the rate was kept unchanged,” said Peiqian Liu, China economist at NatWest Markets in Singapore. “Liquidity is therefore the higher priority for the PBoC.”

Tuesday’s move also signals that the LPR will be kept steady at this month’s fixing on 21 September, as the MLF usually acts as a guide for the LPR. The latter is set by a panel of commercial banks.

“I think last week’s PBoC action is a signal to the market that the central bank is not in a rush to lower the underlying MLF and that targeted easing policy is still preferred because economic recovery is in line with expectations,” Liu stated.

“As a result, it is most likely that the 1-year and over 5-year LPR will be kept unchanged on Monday.”

CHINA ECONOMY: CCP speeds up ‘Digital China’ plan for 100% watch over daily life

“Moreover, the equivalent RRR cut of the liquidity injection has reduced the need for an actual RRR cut, allowing the People’s Bank of China more flexibility to manage interbank liquidity levels,” said Liu. She explained that a RRR cut provides longer-term liquidity relief, compared to the one-year MLF.

Liu expects that the PBoC will remain neutral for the next two quarters and will preserve the use of policy rates for an unexpected economic fall-out. “Until then, fiscal easing will be at the forefront of China’s economic policy, along with a targeted monetary stance, such as targeted RRR cuts for small banks or relending and rediscounting facilities to support the real economy.”

The latest PBoC liquidity injection underscores the PBoC’s commitment to maintaining financial stability and adequate liquidity. The recent performance of Chinese equity and bonds markets reflect a degree of investor confidence in the momentum of China’s economic recovery, and optimism amidst a relative dialling down of the US-China trade dispute in the last couple of weeks, stated Liu.

The yield on China’s 10-year government bond is currently hovering around 3.12%, close to pre-COVID levels.

“China has offered a restrained response to the US’ punitive actions towards China on technology, its handling of the global pandemic, the closure of consulates and China’s stance in Xinjiang, Hong Kong and Taiwan,” said Liu. “In addition, the first phase of the US-China trade deal is making progress, with both US and Chinese officials stating that China is on track to meet its obligations. Finally, China’s real GDP is on track to return to its long-term potential growth rate of approximately 5.5% by Q4.”

As a result, Natwest Markets’ proprietary China Stress Index has gradually eased from a peak of 131 in mid-March, at the height of the coronavirus pandemic, to 101 today, its lowest level since May last year.