Latest consumer and producer price data out of China points to persistent trouble for the world’s second-biggest economy, with analysts cautioning it may be facing a period of “entrenched deflation”.

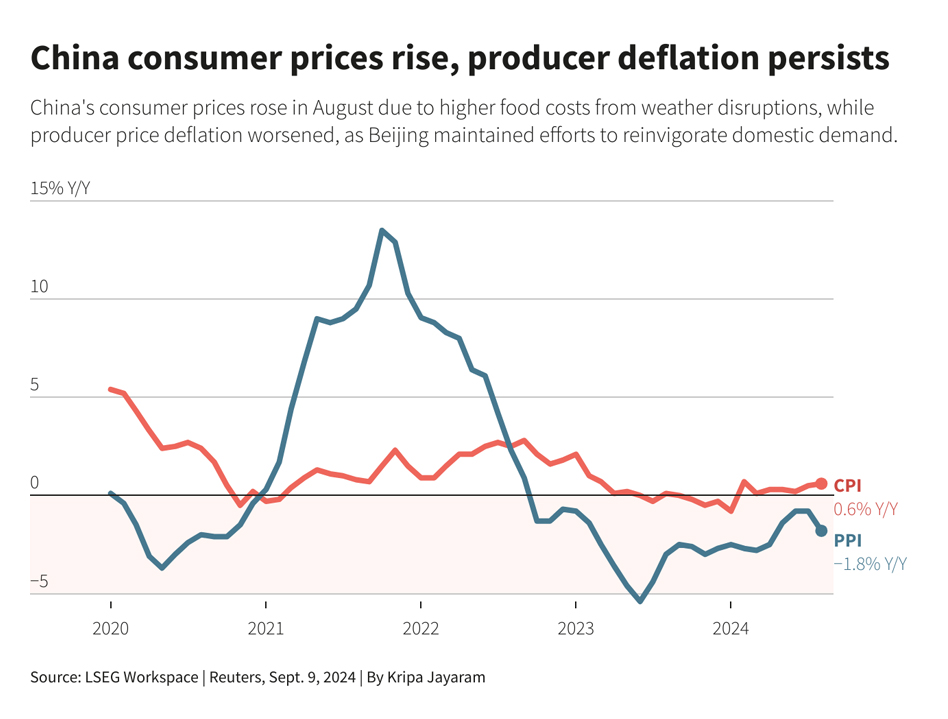

China’s consumer price index inched up slightly, rising 0.6% in August from a year earlier, compared to a 0.5% rise in July, data from the National Bureau of Statistics (NBS) showed on Monday.

The small bump in consumer inflation was still short of economists’ expectations of a 0.7% rise. But that wasn’t the worst of it.

Also on AF: Consumer Confidence in China Drops to Near Historic Lows

A deeper dive into data shows that August’s rise in consumer inflation does not mean much at all.

The higher consumer inflation number is largely down to a jump in food prices due to volatile weather. China is experiencing one of its worst spells of extreme weather this year — with deadly floods and scorching heat destroying crops and pushing up farm produce prices.

Between June 17 to August 15 alone, average wholesale prices for 28 vegetables tracked by China’s Ministry of Agriculture and Rural Affairs jumped by 39.9%, according to state media.

Meanwhile, crops over 1.46 million hectares were affected by various natural disasters in August, state media said.

That would mean the slight uptick in consumer inflation does not point to a recovery in domestic demand, but “continues to mask underlying weakness in price dynamics and domestic demand” in China, Barclays analysts pointed out.

“If we take out the contribution from volatile food prices, we estimate consumer goods inflation was actually around 0%, barely nearly falling into deflation,” Barclays analysts said in a note.

‘Deflation could become entrenched’

Non-food inflation stood at a meagre 0.2%, down from 0.7% in July. Services CPI also fell for the third consecutive month, down to a near-two-year low of 0.5%.

Core inflation, excluding volatile food and fuel prices, was 0.3% in August – the lowest in nearly three and a half years – down from 0.4% in July.

The continued weakness in prices of most non-food segments, including healthcare, recreation, housing and transportation “suggests a risk that deflation expectations could become entrenched,” Barclays analysts said.

Similar concerns were raised by economists at Goldman Sachs and Moody’s, who noted that households were holding back on spending amid a prolonged housing downturn and persistent joblessness.

Economists also highlighted China’s GDP deflator – a measure of changes in price of all goods and service in an economy – has now been negative for five consecutive quarters. That is the longest period of negative readings on record, Barclays noted.

Overcapacity, trade war hurting producers

Meanwhile, the producer price index (PPI) in August slid 1.8% from a year earlier, the largest fall in four months. That was worse than a 0.8% decline in July and below a forecast 1.4% fall.

“The ongoing deflationary pressures boil down into a broader problem of production surplus, which is still outstripping demand,” said Junyu Tan, North Asia Economist at Coface.

A glaring example of China’s excess capacity problem is the country’s solar panel-makers, which have had a dismal first half despite dominating the industry not just at home but also across the world. Net profits at Jinko Solar and Trina Solar, two of China’s biggest solar panel makers, have plunged 69% and 85%, respectively in H1 2024.

The overcapacity is bound to eat into the margins and capital expenditure plans of Chinese firms. And a lack of domestic demand and a global pushback against cheap Chinese exports will continue to exacerbated the problem.

The conditions threaten to create a vicious cycle within China’s economy where demand and supply issues will mean lower employment and wage growth lead to a further fall in private consumption.

“We think the further decline in core CPI/services PPI, and now 23 months of PPI deflation, along with deeper contractions in auto and property sales, deteriorating labour market, and significant negative wealth effects amid falling home prices and stock markets, suggest private consumption will likely weaken further in Q3,” Barclays analysts noted.

Current policies not enough

On the whole, the current scenario points to a huge gap in measures needed to fix China’s spiralling economy.

“We think increased fiscal spending will drive an uptick in domestic demand over the coming months. But government policy is still too skewed toward investment, and so increased fiscal spending may ultimately exacerbate the overcapacity problem,” said Gabriel Ng, assistant economist at Capital Economics.

A national campaign to earmark $41 billion in ultra-long treasury bonds to support equipment upgrades and trade-in of consumer goods has proven lukewarm in spurring consumer confidence, with domestic car sales extending declines for a fifth month in August.

“These policies will take time to filter through, so a demand-led reflation is obviously not yet on the horizon,” Tan from Coface said.

Faltering economic activity has prompted global brokerages like UBS, Goldman Sachs and JPMorgan Chase to scale back their China 2024 growth forecasts to below the official target of around 5%.

Last week, JPMorgan also backtracked on its buy recommendation on Chinese stocks, warning of the risk of a second – and worse – tariff war after November’s US election.

Meanwhile, in unusually strong comments last week, China’s ex-central bank governor Yi Gang called for efforts to fight deflationary pressure on the economy.

“The immediate focus should be that the GDP deflator should be turned to positive. Even if we realise the difficulty of that, we should try our best,” Yi said.

- Vishakha Saxena, with Reuters

Also read:

Chinese Solar Giants’ Profits and Revenue Plunge in First Half

Extreme Weather Cost China More Than $10 Billion In July Alone

China’s Historic Heatwave Turns Deadly Amid Power Crunch Fears

Solar Overcapacity Kills Projects, Fuels Bankruptcies In China

China’s $41-Billion Buy-up of Unsold Homes Seen Falling Flat

China’s Property Sector Will Remain Weak For Years: Goldman

China Starts Merging State Brokerages, to Create $226bn Giant

Beijing Fumes as Canada Slaps 100% Tariffs on China-Made EVs

Chinese Firms Seen Shifting Production Abroad to Avoid US Tariffs