One of the features of the current rally to a record gold price is that it has been driven largely by investment products, with virtually no support from the major physical demand centres in Asia, namely China and India.

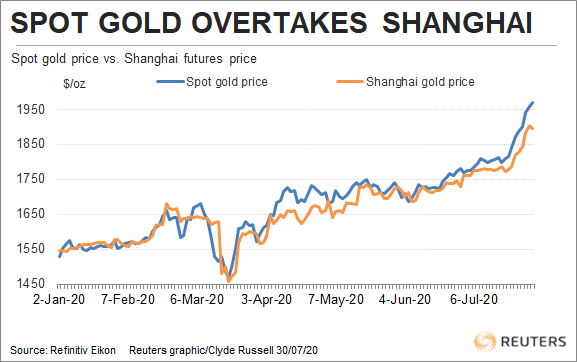

This has resulted in some unusual pricing dynamics, with gold futures in Shanghai trading at a discount to both spot gold and US futures.

The Shanghai contract ended at 426.62 yuan ($61) per gram on Wednesday, which is equivalent to $1,897.10 an ounce.

US futures ended at $1,953.40 an ounce, while spot gold finished the day at $1,970.40, not far off the record high of $1,980.60 reached during Tuesday’s trade.

The Shanghai discount is a reversal from earlier this year, when the Chinese price was at a premium to spot gold.

For example, Shanghai futures closed at the equivalent of $1,629.03 an ounce on March 16, a premium of $115.12, or 7.6%, to the close of the spot price on the same day.

While there are brief periods when the spot price has been higher than the price in Shanghai, the consistent pattern of recent years is for the price in China to trade at a small premium to the international price.

Lower Demand in China, India

The reversal of this dynamic now is most likely a reflection of the lower physical demand for gold in China, largely as a result of the economic lockdowns imposed to combat the spread of the novel coronavirus pandemic.

China’s gold jewellery demand dropped 54% in the first quarter of 2020 from the same period last year, according to Refinitiv GFMS.

While China’s jewellery demand may have recovered somewhat in the second quarter, the weakness in the rest of Asia deepened as the coronavirus spread outside of China and hit economies across the region.

India, the second-biggest gold consumer after China, saw a 64% slump in demand in the first half of 2020, with Refinitiv GFMS data showing imports of only 99 tonnes in the first six months of 2020, down from 436 tonnes for the same period last year.

The coronavirus lockdown and the high price of gold in local currency terms are largely to blame for the collapse in India’s gold demand.

While India is perhaps the worst-hit country among major gold consumers, it’s worth noting that Refinitiv GFMS data show that physical demand was battered across the globe in the second quarter of 2020, sliding 36% to just 677 tonnes, from 1,054 in the same quarter in 2019.

INVESTMENT BOOM

However, flows into investment products such as exchange traded funds (ETFs) soared, jumping 361% to 436 tonnes in the second quarter, Refinitiv GFMS said.

The gold dynamic so far this year is pretty clear, the massive investor interest has been more than enough to outweigh the decline in physical demand.

Ongoing concerns over the global economic outlook, and low to negative real interest rates should serve to keep investor buying robust, even if there is a risk of profit-taking as gold nears the psychological mark of $2,000 an ounce for the first time.

The question of weak physical demand in Asia’s two powerhouse consumers is somewhat trickier.

The most logical expectation is that demand will recover in line with an improvement in the economy, already being seen in China and with some early signs in India.

If this does occur, then gold gets another bullish factor to drive a sustained rally, assuming investor demand continues.

• Reuters

This report was updated on Dec 27, 2021 for style purposes.

READ MORE:

Economic worries return after Fed stoked high