Asian stock markets endured a tough start to the week with worries over China’s economic prospects seeing Hong Kong stocks tank and Japan shares giving up most of their early gains.

The Hong Kong and China sell-off came after Chinese President Xi Jinping chose a leadership team at the twice-a-decade Communist Party Congress that suggested a focus on ideology-driven policies, sacrificing economic growth.

That includes the controversial zero-Covid policy, along with the “common prosperity” initiatives that led to the collapse of the property market and the humbling of China’s tech giants.

Also on AF: China Third Quarter GDP Growth Rises, But Outlook Mixed

Japan’s Nikkei share average gave up most of its morning gains during the afternoon session to close below the key 27,000 level, as investors fretted about the outlook for China’s economy.

Japan’s stock benchmark ended the day up 0.31% at 26,974.90. The broader Topix rose 0.28% to 1,887.19. Real estate was the worst performing sector in the Nikkei, tumbling 2.12%.

The Nikkei had started the day brightly, entering the lunch break 1% higher, buoyed by optimism about a slightly less hawkish US Federal Reserve and the potential for a weaker yen to boost earnings as the corporate reporting season picks up pace this week.

“We need to be wary about downside risks for Chinese growth, this will not be helpful to investor sentiment in Japan,” said Masayuki Kichikawa, chief macro strategist at Sumitomo Mitsui Asset Management.

Hong Kong stocks slid to 13-year lows on Monday and the onshore yuan fell to its weakest level in 15 years after Xi Jinping’s leadership team was unveiled.

The Hang Seng index slumped, touching levels last seen during the 2008-2009 global financial crisis and was 6.36% down at the close, or 1,030.43 points, at 15,180.69.

Hong Kong-listed shares of tech giants Alibaba Group Holding Ltd and Tencent Holdings Ltd plunged 10% and 8% respectively, dragging the Hang Seng Tech Index down 7% to a record low. Hong Kong-listed Chinese developers plummeted 9% to record lows.

Both the property and tech sectors have been targeted for far greater regulation under Xi.

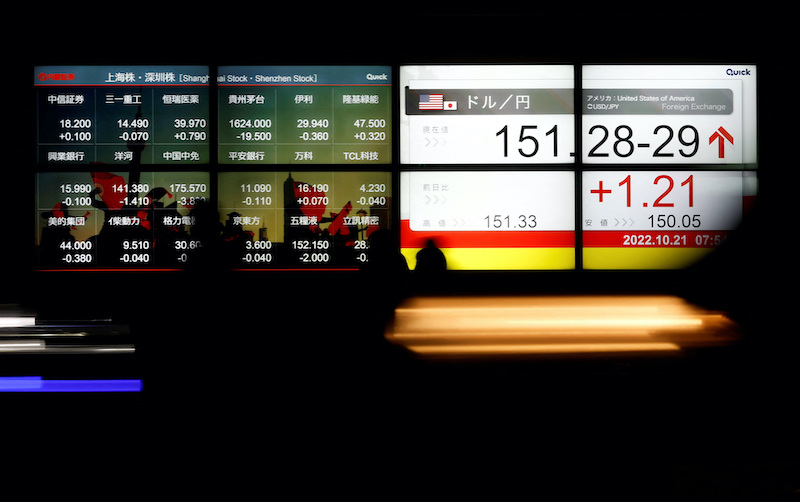

China’s bluechip CSI300 index lost 2.3%, while The Shanghai Composite Index dipped 2.02%, or 61.37 points, to 2,977.56. The Shenzhen Composite Index on China’s second exchange dropped 1.76%, or 34.58 points, to 1,932.34.

Elsewhere across the region, South Korean equities jumped 1% after Seoul said on Sunday its credit support measures will ease worries about a credit crunch in bond and short-term money markets. Indian stock markets were closed for holiday.

Yen Intervention Rumours

Globally, the dollar weathered another suspected blast of Japanese intervention to rise against the yen, while European markets got a lift from hopes that US interest rates could rise more slowly than previously thought.

The dollar roared to 149.70 yen in early trade before hastily retreating to 145.28 in a matter of minutes in what traders and analysts said appeared to be at the hands of the Bank of Japan. It was last down almost 1% at 149.24.

The Financial Times reported the BOJ may have sold at least $30 billion on Friday to try to protect the yen from yet more weakness, which has sharply lifted the cost of Japan’s imports, particularly for resources.

Equities mostly extended the bounce that began late in New York on Friday on talk the Federal Reserve was debating when to slow the pace of hikes and might signal a step back at its November meeting.

Markets are still priced for a rise of 75 basis points next month, but have scaled back bets on a matching move in December. The peak for rates has also edged down to around 4.87%, from above 5% early last week.

Stocks in Europe opened on an upbeat note, with the STOXX 600 up 0.7% on the day, ahead of a week of packed earnings, as 118 companies, including big guns like HSBC, Unilever and TotalEnergies are set to report.

Markets now await figures on US GDP due on Thursday and core inflation measures the day after. The economy is forecast to have grown an annualised 2.1% in the third quarter, while the Atlanta Fed GDP Now indicator rose to 2.9% in the latest week, from 2.8%.

Sentiment will also be tested by some major earnings with Apple, Microsoft, Google-parent Alphabet and Amazon all reporting.

Key figures

Tokyo – Nikkei 225 > UP 0.31% at 26,974.90 (close)

Hong Kong – Hang Seng Index < DOWN 6.36% at 15,180.69 (close)

Shanghai – Composite < DOWN 2.02% at 2,977.56 (close)

London – FTSE 100 < DOWN 0.62% at 6,926.55 (0935 BST)

New York – Dow > UP 2.47% at 31,082.56 (Friday close)

- Reuters with additional editing by Sean O’Meara

Read more:

Unveiling of ‘Team Xi’ Spurs Hong Kong Stock, Yuan Plunge

China’s New Leaders Unveiled in Beijing, Li Qiang No-2