(ATF) Asian equities peaked twice in the first quarter amid optimism over the recovery in China, the prospect of improved relations between the new US administration and China, and the arrival of COVID-19 vaccines. But the outlook for much of the region remains positive, even after a valuation-related stumble, according to Zhikai Chen, head of Asian equities at BNP Paribas Asset Management.

How have Asian equities responded as the reflation trade took hold?

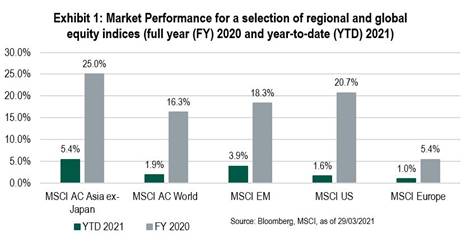

It is true that Asian market have had a volatile couple of months after peaking twice in the first quarter as percentage returns approached the ‘teens’ (see Exhibit 1 below for performance of Asian and non-Asian equities in 2020 and 2021 year-to-date). Those highs were followed by a reassessment of valuations as US bond yields began to rise over market concerns that inflation would take off as the economic recovery took hold and accelerated. Such a view has particularly affected growth markets such as Asia, causing capital flows to reverse as investors reassess the outlook for growth stocks in a rising rate environment.

The good news, however, is that earnings growth has been robust. Growth rates have been good and not just because we are coming off a low base. Companies are delivering earnings growth on an ongoing basis. In my view, that contributes to a good earnings and cash flow outlook.

Are investors differentiating between the prospects for countries that have managed the Covid crisis well and those that have not?

They certainly are. We have seen a shift in capital flows in recognition of this assessment and the fact that Asia remains a key factor for the world when it comes to manufacturing. It has a central role in supply chains and decoupling is not an easy option.

Of course, we have to distinguish between north Asia and south Asia where countries in the north have done well while southeast Asia and India lag behind. In the north, mobility levels are back to pre-pandemic levels, the hospitality sector has reopened, spurring the recovery. That is where capital is going to flow to.

In addition, over the last 12-18 months there has been a very interesting development as Asia has become a key hub for semi-conductors. There have been shortages due to a lack of capacity. I would expect capital inflows in this area to reinforce Asia’s capacity to produce semi-conductors.

Beyond volatility, what other risks do you see?

We believe it is important that as investors we understand exactly what companies we are buying: the sector outlook, their vulnerabilities to another shutdown and their potential exposure to a recovery.

At the macroeconomic level, we have seen a reassessment of central bank policy and the outlook for interest rates after the recent rise in US bond yields. This has caused investors to think about valuations and reconsider whether they are appropriate.

We are continuing to take a cautious view. We will not rush back into some of the beaten-down sectors, even though valuations have fallen. There is a lot of optimism about the outlook over expected developments such as vaccine passports, but we remain wary of false dawns.

What sectors do you consider attractive?

To start off, we are fundamental investors. The market may still look challenging from a price level perspective. However, we are comfortable with companies’ earnings growth and cash flow potential, given what we know about fundamentals such as supply lines and contract fulfilment. That leaves us confident about our choices, which are not based on hope but solid fundamentals as illustrated in the below chart.

Source: BNP Paribas Asset Management, 2021

Naturally, we like the consumer sector, which should benefit from the ongoing recovery and the continued boom in e-commerce, but also financials which look promising given the expected profit rebound, improved loan growth and stabilising margins.

We expect the information technology sector to benefit from the global shortage of semiconductors. In this area, Asia has become the manufacturing hub and we expect companies with solid pricing power to benefit, particularly as capital flows there to help boost supply.

READ MORE:

Asian equities advance but inflation and correction worries persist