Shares and bonds of Chinese property companies fell further on Wednesday after China Evergrande Group missed a third round of interest payments on its dollar bonds in three weeks, and as others warned of defaults.

In the clearest sign yet of global investors’ worries of spreading debt contagion, the option-adjusted spread on the ICE BofA Asian Dollar High Yield Corporate China Issuers Index surged to a fresh all-time high of 2,337 basis points on Tuesday evening US time.

On Wednesday morning, Shanghai Stock Exchange data showed onshore bonds issued by developers Shanghai Shimao Co Ltd and Country Garden Properties Group were among the biggest losers on the day, falling between 1% and 4.2%.

A sub-index tracking A-shares of property firms fell 1.58% against a 0.31% rise in the blue-chip CSI300 index.

Markets in Hong Kong were closed on Wednesday morning due to a typhoon affecting the city.

Long drawn-out restructuring

Evergrande did not pay nearly $150 million worth of coupons on three bonds due on Monday, following two other missed payments in September. While the company has not technically defaulted on those payments, which have 30-day grace periods, investors say they are expecting a long and drawn-out debt restructuring process.

The company’s main unit, Hengda Real Estate Group Co, faces a 121.8-million yuan onshore bond coupon payment on October 19 and Evergrande has another $14.25 million dollar bond coupon due on October 30.

Debt pressures extend far beyond Evergrande. Chinese property developers have $555.88 million worth of high-yield dollar bond coupons due this month, and nearly $1.6 billion due before year-end, and Refinitiv data shows at least $92.3 billion worth of Chinese property developers’ bonds maturing next year.

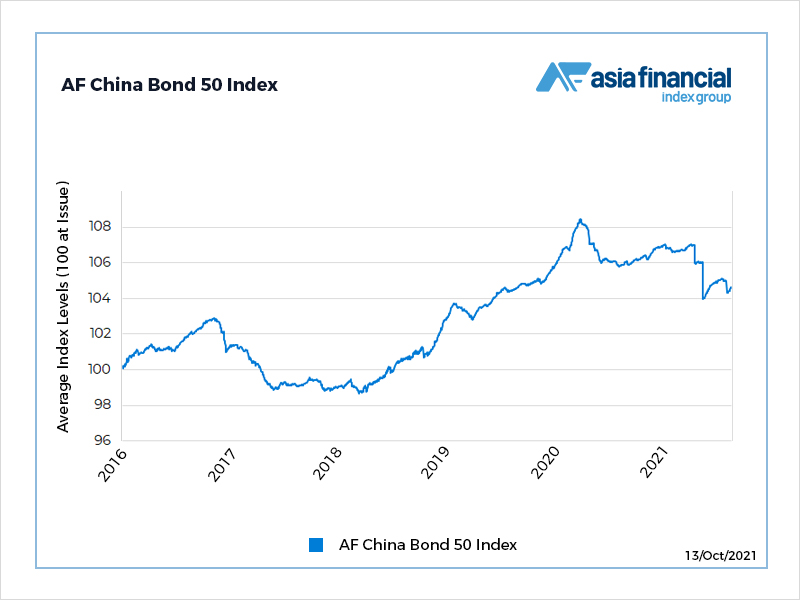

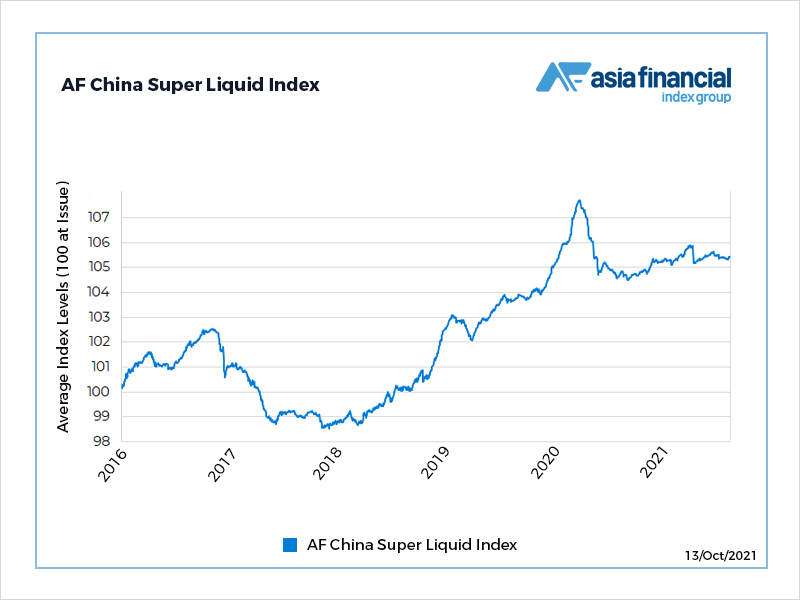

And while the contagion has been, so far, largely contained within the high-yield sector, some knock-on effects are evident even in the AF China Bond 50 index – see the chart above – which has no property companies among its constituents and is dominated by triple-A credits. The AF China Super Liquid index – see below – has fared a little better, in large part because it includes government-issued bonds that act as an additional buffer for investors. Both indexes are owned by Asia Financial’s parent, Capital Link International.

Overshooting deadlines

Evergrande’s mid-sized rival Fantasia has also already missed a payment and Modern Land and Sinic Holdings are trying to delay payment deadlines that would still most likely be classed as a default by the main rating agencies.

“These stories have challenged the notion that Evergrande is one of a kind,” analysts at Capital Economics wrote in a note.

While China’s policymakers will likely be able to avoid a “doomsday scenario” the overextended property sector will continue to weigh on the world’s second-largest economy, they said.

“Even following an orderly restructuring of the worst-affected developers with minimal contagion to the financial system, construction activity would still almost inevitably slow much further.”

The IMF said on Tuesday that China has the ability to address the issues linked to Evergrande’s indebtedness, but warned that an escalation of the situation could lead to the emergence of broader financial stress.

- Reuters with additional editing by Jim Pollard