(ATF) China’s 4.9% year-on-year third quarter 2020 GDP growth was lower than my 5.5% forecast. But the new data (released on 19 October) has not changed my fundamental case and forecast trajectory that China’s recovery started after the growth plunge in the first quarter and the second quarter was a V-shaped rebound from that bottom.

Data since 2Q20 shows continued and steady recovery. I now expect full-year 2020 GDP growth at 2.2% year-on-year (versus 2.3% before) and 6.6% YoY in 2021 (same as before), and continue to expect the recovery to peak in the first quarter of 2021.

In a nutshell

The PBoC has ended its easing since 2Q20 and put policy on hold. Its next move is data-dependent. Credit growth is about to peak soon, though monetary tightening is not yet in sight. China Government Bond yields have risen since the 2Q data were released. Yields may have plateaued and be range-bound between 3.0% and 3.5% in the coming year. A non-inflationary moderate growth environment with supportive policies are positive for Chinese stocks in 2021.

China’s growth recovery will benefit global growth. The IMF expects that China would be the only major economy in the world to show positive growth in 2020 and its contribution to global growth would increase from an estimated 26.8% in 2021 to 27.7% in 2025. But despite this, in my view, one should not expect China to boost significantly commodity and energy prices, as its demand intensity for these products has entered a secular slowdown.

How different is this recovery?

The economic recovery is on track and broadening out to the demand side, correcting some of the lopsided recovery problem that the production side was the sole growth driver in 1H20. But the demand recovery has remained sluggish, with retail sales rising by only 3.3% YoY in 3Q20 which was less than half the growth pace of the production and investment indicators.

China’s has regained its output losses due to the Covid-19 shock, with GDP 0.7% higher than a year ago on a year-to-date basis. That is why the authorities are happy with the recovery pace and have stopped easing.

China’s quick recovery is a product of its stringent lockdowns, massive testing, infection tracing, a large domestic economy supported by fiscal and monetary stimuli. Export growth is a bonus but it is not expected to outperform for too long. Continued domestic-driven recovery is expected in the coming quarters, with growth in the service sector and consumption catching up.

Crucially, the recovery has come with relatively restrained policy stimuli compared to both China itself and other countries. Beijing has focussed on targeted easing with much less public investment this time around than in the past cycles. The policy on boosting the new sectors, such as technology, services and consumption upgrading has improved GDP growth quality, making the economic recovery sustainable.

Impact beyond China’s borders

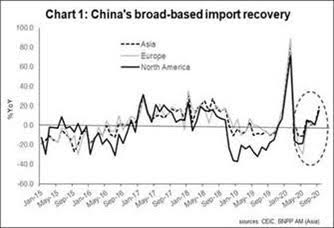

China’s import recovery has benefited the global economy, with the impact spanning from Asia to Europe and the US (Chart 1).

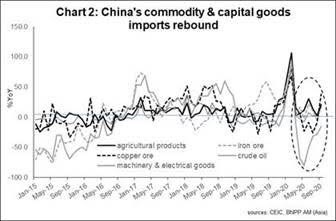

Commodities and capital goods imports, including iron ore, crude oil, copper, agricultural products and mechanical and electrical goods, also rebounded, thanks to the recovery in domestic demand (Chart 2).

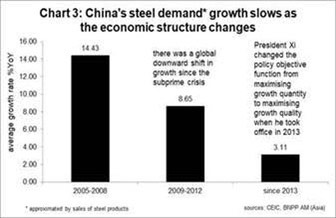

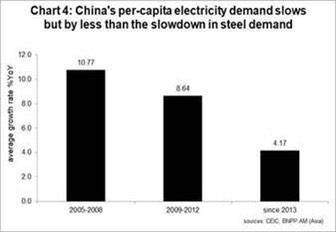

However, the market should be realistic about China’s demand for commodities, as its energy and commodity demand intensity has been falling (Chart 3 & 4) due to economic restructuring to move the economy away from industrial-based investment-led growth to service- and tech-based consumption-led growth. China’s commodity and energy demand will recover along with the economy, but super-strong demand growth rates like those in the 1990s and 2000s are gone for good.

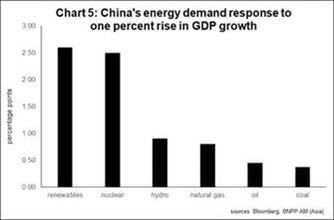

Empirical evidence shows that in the past decade, every one percentage point rise in China’s real GDP growth would create 0.55% growth in overall energy demand. Based on my forecast of 2.2% YoY GDP growth for this year, overall Chinese energy demand would grow by just 1.2% YoY (versus 4.2% YoY growth in 2019). Furthermore, most of the energy demand will come from renewals, such as wind, solar, hydro-electric, nuclear and natural gas (Chart 5) due to the government’s renewable policies.

Policy and market outlook

Credit growth in China is peaking soon as the economic recovery from the pandemic consolidates. The PBoC has put monetary policy in neutral gear; the next policy move is data-dependent. If economic growth disappoints, there will be more policy easing (probability 20%, in my view). A disinflationary steady growth environment is positive for Chinese equities in the coming year.

Recent market research shows an increasing willingness by Chinese household to increase equity exposure. Foreign portfolio inflows to China are expected to continue due to addition of Chinese stocks and bonds to international benchmarks, among other factors. The latter will improve market sentiment on Chinese assets.

Chinese bond yield has plateaued and is expected to range between 3.0% and 3.5% in the coming year (CGB 5-year yield is at 3.07% at the time of writing). This takes into account steady growth allowing Beijing to resume its deleveraging policy and retreat from implicit guarantee to let the zombie companies exit the system. In my view, the PBoC’s policy is to facilitate financial reform while containing systemic risk and preventing bond yields from moving beyond this expected range.