Chinese authorities played their cards better on day-2 of their annual parliamentary get-together, the National People’s Congress, in Beijing on Wednesday.

There was a strong negative reaction to news on Tuesday that new Premier Li Qiang would not be giving a press conference at the end of the current congress – a move which ended a 31-year tradition to explain the country’s economic policies to the media and the general public.

But on Wednesday, the country’s leadership, mindful perhaps about the economic slowdown and the importance of revving the economy up, wheeled out its economic heavyweights to reassure both Chinese citizens and international investors, about its economic strategy for the year ahead.

ALSO SEE: US House Panel Set to Consider New Bill That Could Ban TikTok

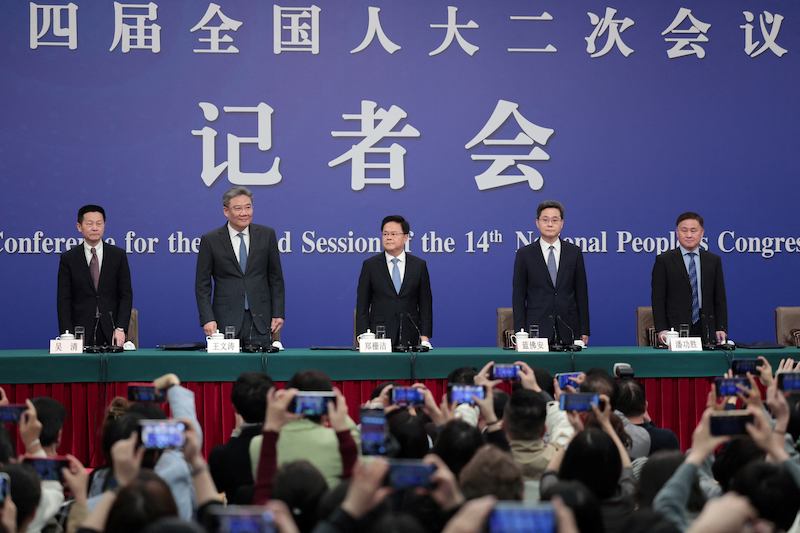

China’s finance and commerce ministers, plus heads of the central bank, the National Development and Reform Commission and China Securities Regulatory Commission, all took the stage in Beijing to reinforce the message that the country is serious about repairing its economy.

Zheng Shanjie, head of the NDRC, was one of the first to answer questions, saying that while China’s GDP growth target of 5% was ambitious, it fitted with the country’s 14th five-year plan and “can be reached with a jump.”

Zheng said China’s “new three” exports – electric vehicles, lithium-ion batteries and solar panels – showed the strength of China’s manufacturing capacity. “The overall growth has been 30% from the year before,” he said, in comments published by the South China Morning Post.

“This exemplifies that China is accelerating its transition from old to new economic engines, and that our manufacturing quality keeps improving,” he said. “Such high-quality development of our manufacturing sector will bring new drivers to the market.”

Meanwhile, power generation in January and February this year was up 11.7% from 2023. That showed China’s recovery was on an increasingly solid footing and the economy resilient. Special bonds, consumption support measures and tax reductions would help “fight unpredictable external factors”.

Of course, there were “immense business opportunities for overseas investors”, but Zheng also noted the country faced several potential roadblocks – “an increasingly challenging external environment”, strong competition and business risks in some sectors, plus difficulty setting up a unified domestic market.

“These problems only emerge because we are progressing. They will be solved as we continue to develop.”

A more convenient investment environment would be created for private businesses by giving “more space, lower cost” to efficient investment.

Tax cuts for tech, incentives to boost consumption

Finance minister Lan Foan said China would offer tax cuts for tech innovation and the manufacturing sector this year, while Commerce minister Wang Wentao said two moves would be implemented to boost consumption – offering incentives for citizens to replace used cars and home appliances, and boosting services consumption.

Pan Gongsheng, governor of the People’s Bank of China (PBOC), said China had ample room and a deep toolbox for monetary policy.

China could afford to make further cuts to its reserve requirement ratio, he said, as the country’s RRR average of 7% was still high compared with other countries.

He said the central bank would also look at stabilising price levels and pushing for a small rebound in prices, as the country has faced increasing deflationary pressure since late last year because of weak domestic and foreign demand.

The yuan exchange rate could be kept stable, he said, because a policy turnaround was widely anticipated in developed markets, which would reduce the momentum of the US dollar and boost China’s fundamentals.

Pan said loans would be used to support tech innovation and renovation, while lending would be restricted to sectors at over-capacity.

The NDRC’s Zheng said the large-scale trade-in programme for home applicances could be a big deal as that was a multi-trillion-yuan market, and that would be a boost for consumers and manufacturers. Research had shown there were at least 336 million vehicles and 3 billion washing machines, refrigerators and air conditioners in the country.

Finance minister Lan Foan said the government had cut admin costs by 20% last year and that “belt tightening” would be a long-term effort. But they would “splurge” when necessary, with a “more focused” use of resources.

The government was ready to boost support in sectors such as science and tech development, which he said had risen by 30% over the past five years.

Wu Qing, the new head of the China Securities Regulatory Commission, said he was focused on “open and just” regulation and would protect small investors.

It was important to make capital markets more “transparent and fair”, he said, so he would try to protect the rights of small and mid-sized businesses.

Cracking down on fraud, market manipulation and backdoor trading would also be a priority. If the quality of listed enterprises and their IPOs could be raised, investments would be more efficient.

They would conduct more checks on companies that seek public listings, plus regular checks on listed companies to try to curb illegal activities such as fraud and money trapping. Meanwhile, the country needed effective regulation of quant trading to ensure the market is fair and provides value.

- Jim Pollard

Note: Minor edits were done on the text and a link added on March 6, 2024.

ALSO SEE:

Chinese Investors Plough Into Offshore Assets, Hit Outbound Limit

Doubt on China’s Plan to Lift Consumption, Maintain Growth

PM Pledges to Revitalize China’s Economy, Aims at 5% Growth