It’s not a good sign for any economy when debt collectors are booming and in China right now, the industry is on a hiring spree.

Whole Scene Asset Management, a debt recovery firm based in the southern province of Hunan, plans to double staff numbers to 400 people this year as it expands into new cities.

“Debt collection companies have been mushrooming,” company founder Zhang Haiyan said. “And with bad loans growing this year, everyone is adding new hands.”

Rival Bricsman is also hiring – hoping to boost headcount of around 1,000 by 400-500 this year after landing a deal to collect delinquent consumer loans for China Minsheng Bank, people with knowledge of the matter said, declining to identified as they were not authorised to talk to media.

Bricsman, which is based in the eastern province of Jiangsu and counts other large banks amongst its clients, did not respond to a request for comment.

As increasing numbers of consumers struggle with lost income in an economy battered by the coronavirus and US-China tensions, a burgeoning wave of non-performing loans is sparking concern among lenders – both at specialist consumer financing firms and traditional banks – and even among debt collectors.

China is the midst of “an unfolding debt crisis”, says Joe Zhang, a business consultant and until last month vice chairman at the country’s largest debt collector YX Asset Recovery.

The delinquency rate for consumer debt is climbing and collecting on those loans has become much harder, he added, estimating that at some weaker non-bank consumer lenders, soured loans may account for 30% to 50% of their portfolios.

That bodes ill not only for Beijing’s efforts to spur domestic demand but also for the financial health of consumer lending firms which help provide credit seen as vital for shoring up the pandemic-hit economy.

Strategy rethink

The China Banking and Insurance Regulatory Commission did not respond to a Reuters request for comment on its current assessment of risks posed by soured consumer loans.

It last said delinquency rates were under control when it noted a 0.13 percentage point rise in the non-performing loan ratio for first-quarter consumer debt compared to the start of this year. But that data only captures bank loans and not those extended by the country’s vast numbers of specialist consumer finance firms including micro lenders.

Even at banks, which generally have stricter loan criteria, concern is building.

An internal review by Bank of Shanghai Co Ltd saw its non-performing loan ratio for consumer debt soar in the first quarter, said a company source familiar with the matter.

“We’ve already started to reduce our exposure in consumer finance by cutting our co-lending business with smaller platforms,” said the source, who like other lending sources was not authorised to speak to media and declined to be named.

Bank of Shanghai did not respond to a request for comment.

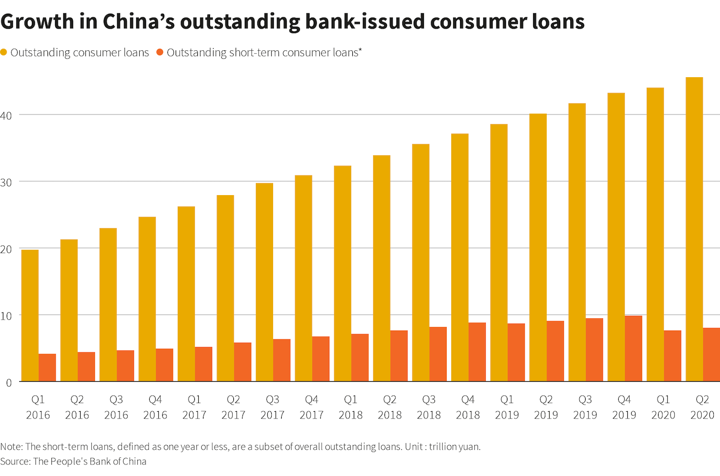

Chinese consumer debt has ballooned over the past five years, fuelled in part as banks scrambled to issue credit cards, with outstanding debt for bank-issued cards doubling to 17.6 trillion yuan ($2.5 trillion).

Internet-based consumer financing, which is only lightly regulated, has also grown – by a dizzying 400 times to nearly 8 trillion yuan since 2014, according to the Guanghua School of Management.

And Chinese household debt – including mortgages and unsecured consumer loans – has swollen to levels equivalent to nearly 60% of GDP, up from 18% in 2008, the peak of the global financial crisis.

Like Bank of Shanghai, some lenders are rethinking their retail strategy.

China Merchants Bank, which derives about 55% of its business from individual clients, is reviewing an earlier plan to increase that portion of its business to 60%, its president Tian Huiyu said in April after its first-quarter earnings.

Shanghai ShangCheng Consumer Finance has lifted its thresholds for new borrowings while intensifying debt recovery efforts, a company manager told Reuters.

Shanghai ShangCheng did not respond to requests for comment.

“Most licensed non-bank consumer finance firms in China lost money in the first half,” the manager said, adding that many smaller firms will “need capital injections to keep afloat or they will face liquidity pressure when they write off huge amounts of soured debt.”

(Reporting by Samuel Shen in Shanghai and Cheng Leng and Ryan Woo in Beijing; Editing by Edwina Gibbs)