Exchange-traded funds and foreign mutual funds that invest in Chinese yuan bonds saw a record outflow – of $2.3 billion – in the week to May 18, according to data from Refinitiv Lipper.

The rise in US bond yields plus the weakening of the Chinese currency were key factors in the ramp-up in selling by foreigners.

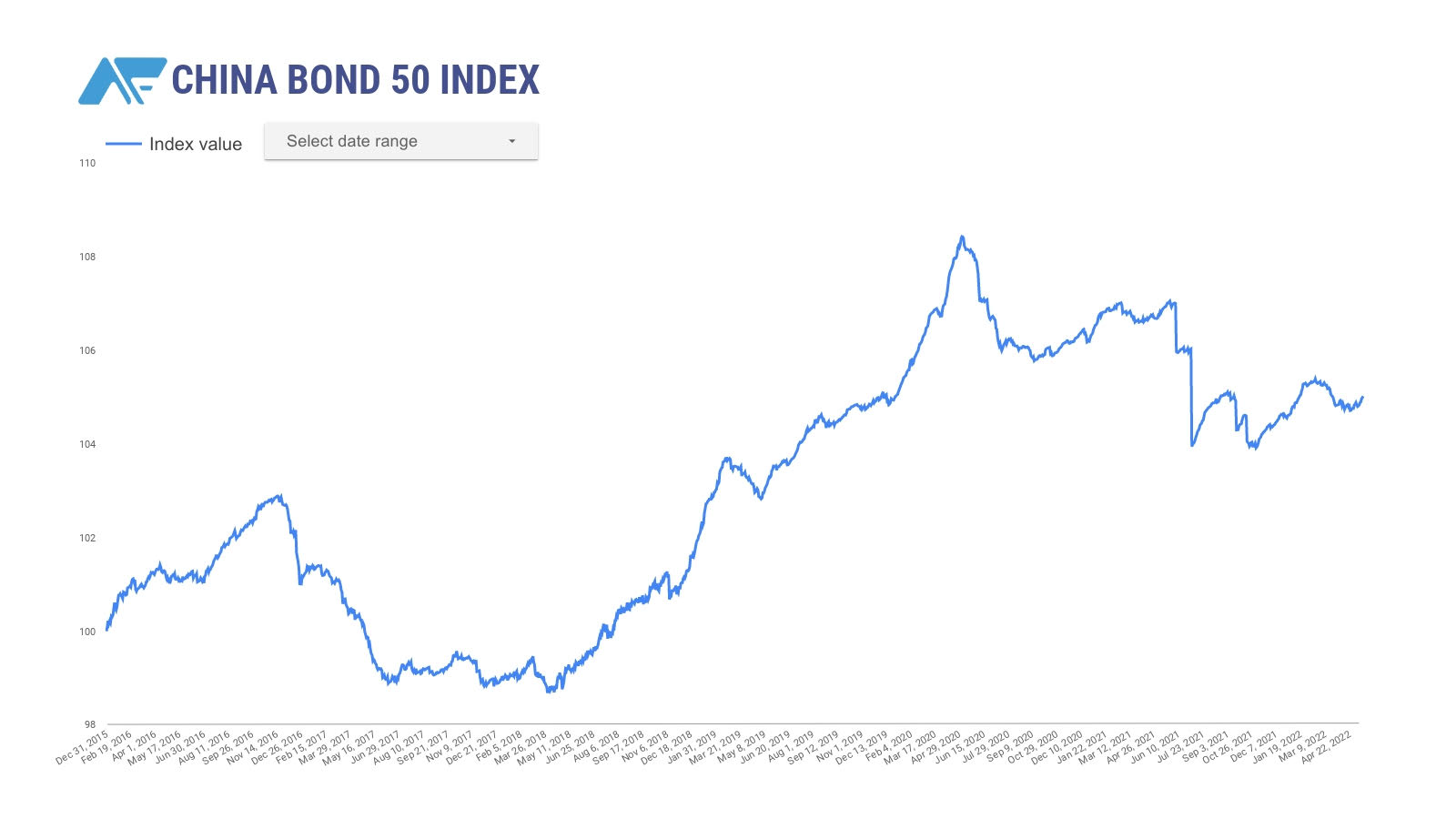

Foreign investors have sold yuan-denominated bonds aggressively over the past three months, bringing down their total holdings to $558 billion at the end of April, a 2.8% decline from March.

Ashish Agrawal, head of emerging markets macro strategy in Asia, estimated that there was about $10 billion in foreign outflows from Chinese bonds in May.

“Active foreign investors could continue to reduce their exposure, with duration and FX returns less of a driver as rising global yields provide other carry alternatives,” he said.

However, he doesn’t expect this pace to be sustained in the second half of the year as the bulk of holdings reflect reserve manager, sovereign wealth fund and index tracking demand.

ALSO SEE: Beijing Residents Told to Keep Working From Home as Cases Rise

US Rate Hikes

The iShares China CNY Bond saw net sales worth $553 million in the week to May 18, while iShares China CNY Govt Bond and HSBC China Government Local Bond Index fund saw outflows of $396 million and $266 million respectively.

At the start of the year, China’s 10-year government bonds offered a solid 1.1 percentage point yield premium over US 10-year government bonds. However, that premium has evaporated in the past few months, thanks to the Federal Reserve’s aggressive interest rate hikes and its tough stance to combat soaring inflation.

China’s 10-year bonds now yield slightly less than their US counterparts.

China’s yuan has also slumped about 4.5% so far this year against a high-flying dollar, hit by concerns over slowing economic growth that have been exacerbated by widespread strict lockdowns aimed at curbing the spread of Covid-19.

At the end of last week, China cut its 5-year loan prime rate (LPR) much more than expected in a bid to boost the housing sector, but kept its 1-year LPR unchanged.

“The intact … 1-year LPR fixing showed China is still concerned about the impact of inverted China-US yield differential and uncertain inflation outlook,” OCBC said in a note on Monday.

“Given the Fed is expected to deliver another 100bps rate hike in June and July, the outflow [from Chinese bonds] may continue for a while in line with other emerging markets.”

• Reuters with additional editing by Jim Pollard

ALSO on AF:

China’s Yuan at Two-Week High as US Ponders Tariff Cuts

China Offers Easier Capital Market Access to Covid-Hit Firms

Chinese Investors Avoid Stocks, Opting For Bonds, Deposits