Chinese consumers have a reputation for deep pockets and broad shoulders.

During the Great Recession, the global economy was propped up by their spending power after the 2008 Financial Crisis threatened to rip it apart. But this time, the “US$4.9 trillion-force” could buckle under the strain of the Covid-19 pandemic.

“Debt has always been a concern hovering [around] the Chinese economy. For [a] long [time], the goose that laid the golden eggs has been abundant household savings and the low indebtedness, but things have changed,” Natixis, the French corporate and investment bank, stated in a report entitled Covid-19 Uncovers China’s Household Debt Accumulation And Its Risks.

“Household debt grew from 28% in 2011 to 55% in 2019 as a share of GDP [gross domestic product] with an average yearly growth of 19%. The coronavirus outbreak has only exacerbated an existing problem,” the study released last week and compiled by Alicia Garcia Herrero, Jianwei Xu and Gary Ng said.

Right now, cash-strapped Chinese consumers are not what the world is looking for. More than 1.8 million people across the planet have been infected by Covid-19 with the death toll edging past 114,000.

Business activity has barely registered a heartbeat, while the word lockdown has become part of the lexicon of life. In response, global governments have injected $8 trillion into the system to shore up creaking economies.

Still, the International Monetary Fund has warned that the world could be facing the deepest peace-time recession since the 1930s. A report by JPMorgan Chase, the investment bank, has also suggested that dwindling output could wipe out $5.5 trillion, or almost 8% of GDP, by the end of 2021.

Hardly surprising then that all eyes have turned to the Chinese consumer. At home and abroad, the country’s middle class has become a giant cash machine. But that was before debt caught up with “household” spending.

‘Annual growth’

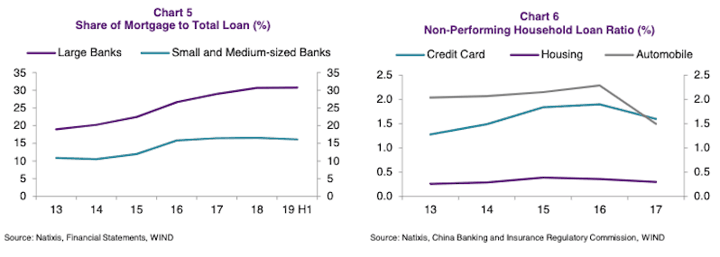

“Among different types of household debt, mortgages are the key component with average annual growth at 22% from 2015 to 2019. In the past, higher mortgages mirrored China’s property boom. But the economic deceleration with weaker home prices mean mortgages are mounted for different reasons . under a stagnant housing market,” the Natixis study said.

“We do not think financial stability risks related to mortgages are immediate for banks as they continue to be safer assets than credit cards and auto loans. But the situation could deteriorate rapidly if the property market encounters a negative shock. The risk is bigger for large banks as their share of mortgages to total loans surged from 20% in 2013 to 31% in [in the first half of 2018] while the ratio only increased from 11% to 16% for small- and medium-sized banks,” it added.

But a depressed “housing market” is only part of the problem. Credit card debt looks certain to radically reshape spending habits, while the fallout will have global consequences once the world opens up again after the Covid-19 crisis.

In 2018, Chinese consumers spent $277.3 billion during overseas trips, which was an increase of 5.2% compared to the previous year, the World Tourism Organization highlighted. For the first half of 2019, “outbound trips increased by 14%.” Balancing household budgets will become a priority even if the coronavirus outbreak is brought under control in the next few months.

“The most immediate risk to financial stability stemming from household debt clearly lies on credit cards. Although the growth on short-term consumption loans has decelerated so far in 2020 and the delinquency rate has declined over years, the situation is likely to deteriorate due to the halt of economic activities caused by [the] coronavirus, and more importantly household income,” the Natixis report stated.

-

![]()

Graphics from a report by Natixis about China’s household debt. Graphics: Natixis

Indeed, this comes at a time when China is desperate to boost consumer spending. The world’s second-largest economy was brought to a standstill by Covid-19 earlier this year after reporting the first official cases of infection in Wuhan, the capital of Hubei province, in January.

Since then, the aftershocks have been horrendous.

Last month, data from the National Bureau of Statistics showed that industrial production for January and February dropped by 13.5% for the first two months of the year compared to the same period in 2019. Retail sales also plunged by 20.5%. The record-breaking fall continued when it came to fixed asset investment, which plummeted by 24.5%.

To complete an appalling set of figures, profits at industrial firms during the same period slumped 38.3% from a year earlier to 410.7 billion yuan or $58.15 billion. Moreover, that was the lowest level recorded in a decade.

Amid this economic environment, China’s ruling Communist Party governmenthas moved to stimulate retail sales by offering online vouchers worth billions of yuan to shoppers. The private-public partnership scheme involves Alibaba and Tencent, the big beasts of the e-commerce world.

Consumers can pick up free digital vouchers through payment platforms such as Alipay and WeChat Pay.

“We are directing local governments to implement policies to expand consumer spending . and also support local governments launching pragmatic and effective measures in a targeted manner,” Ha Zengyou, the deputy head of the employment and income distribution department at the National Development and Reform Commission, said.

For now, the jury is out on whether it will be enough to kickstart a spending spree in China. As for the rest of the world, a middle class weighed down by debt is bad news for the global economy.