(ATF) The special purpose acquisition company (SPAC) market is to me one of the major focal points going forward for a host of reasons. Why are SPACs so trendy and will this trend last for a long time? Or is this another bubble that will end in tears? It certainly has many bubble qualities, but in a perverse way that may be a good thing – an important consideration for establishing a pricing gauge.

One needs a broad array of good, bad and indifferent products in order to create a valuation scale and risk pricing. Without failures the market can’t gauge success nor value the spectrum. There will be many horrible failures. Not because the mechanism or structures are bad, but because the operators are – just like defaults are important in credit markets for accurate resource allocation.

Those with weak projects must pay a higher price. There are probably 50-plus SPACs that don’t have proper human capital in place and will not only face full redemption but may pull out many other not-so-commonplace salvage tactics that will leave many in their wake. But this is part of building a rating backdrop to properly price risk and understand forward valuation.

Here is why the SPAC market and mechanism is very important to the market. SPACs as a whole return about 5% per year – certainly more than US Treasuries or Chinese government bonds and they even seem to have stolen gold’s thunder. With unprecedented quantitative easing from the central banks, huge excesses of cash are looking for homes, returns and safe havens. The SPAC market is the primary beneficiary. Is this good or bad? Probably neither – it’s just a fact.

So, it could show the pulse of investors and clearly reflects sentiment – a view into the soul of the investors. Large sums of money chasing the future when there is very little information about the future or the boundaries (blank cheque requisite) are speculative by definition. The speculation, though, is different than what we have seen in, say, 2000 during the dotcom bubble, as it’s an accelerant this time. It’s now the perfect marriage candidate for private equity.

Exit strategies

Private equity has been inverting company evolution for some time now in the sense they have defined the finish line before, in most cases, defining the starting point. The finish line being an exit strategy. You build a concept to exit to a predetermined goal normally called an initial public offering.

That strategy has been wildly successful for the chosen few but very challenging for the vast majority, ending in a lot of failed businesses.

So, as we merge the ingredients in front of us, we have two very helpful components that help augment growth and value in the private market: Huge sums of money supporting the growth of private enterprises and a newly-formed exit mechanism that fits perfectly to the private to public process necessary to complete the cycle.

The US Federal Reserve’s priming of the pump has helped fuel the private market surge with more money flowing to help extend gestation periods and trial and error that was once highly defined in time by the finite capital pool. The pool now seems infinite, thus the companies are getting longer time, more support and more flexibility to scale. This is an unintended but positive consequence of monetary easing.

This phenomenon without a proper and deep exit opportunity would be very problematic. But 180 SPACs looking for business combinations could come to the rescue; a marriage made in heaven but a union requiring caution. Prudence needs to prevail as there are many unfit for purpose and incapable of completing the full cycle.

Also, we seem to be in the early process of sharpening the valuation matrix’s currently being applied to concepts, meaning “I have a dream” business plans.

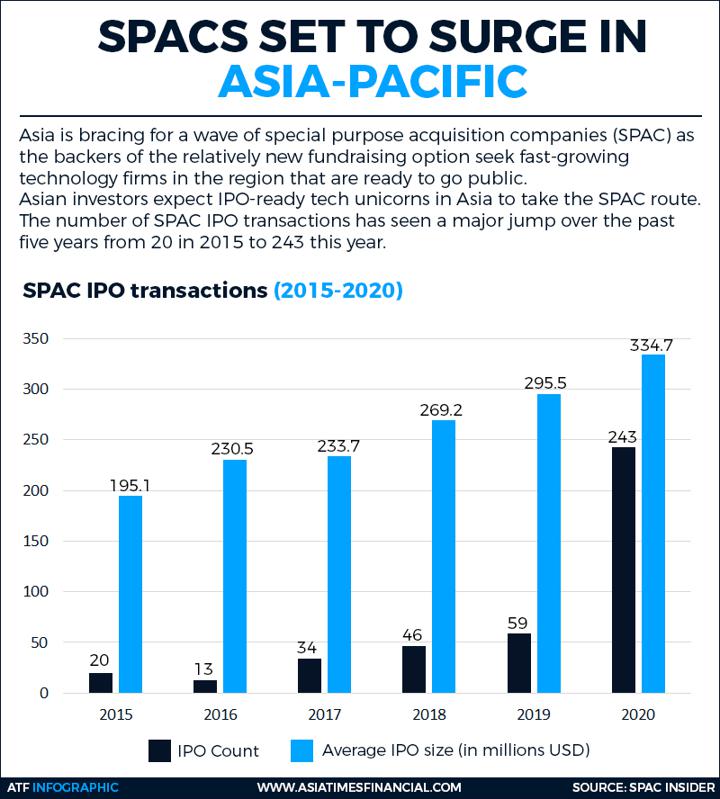

The last component that maybe the most important is the evolution of Asian private companies with a focus on Chinese start-ups. With many US firms heavily picked over, business combinations will look abroad – mainly to Asia. Listing rules in both China and Hong Kong will see many Chinese start-ups list via SPACs in the US.