The Bank of Japan (BOJ) seems to have scored an interim win in its long-drawn battle with bond bears.

The policy meeting held by the Japanese central bank this week seemed, initially, to be a damp squib for excited markets, given it defied expectations for change by maintaining its cap on 10-year yields and modified a funds-supply operation such that offers more money for longer tenors to banks.

But the moves have chilled speculators who have for months been short-selling Japanese government bonds (JGBs), betting that rising inflation and dislocations caused by its massive market interventions will soon force the BOJ to alter or abandon its yield-curve-control (YCC) policy.

“A lot of hedge funds that bet against 10-years decided to cover, as they were surprised by the BOJ funding programme,” said Tadashi Matsukawa, Japan head of fixed income investments at PineBridge Investments.

Matsukawa said he squared his pure short JGB positions to take profit ahead of the BOJ meeting and is neutral now.

“Currently there is uncertainty and the market will be very volatile. I will not be taking many risks,” said Matsukawa.

Yet he expects the BOJ to abandon YCC eventually, and says he will be readying for that, waiting to see when speculators return to sell JGBs again.

ALSO SEE:

Japan’s Car, Chip Exports To China Slump, Fuel Slowdown Fears

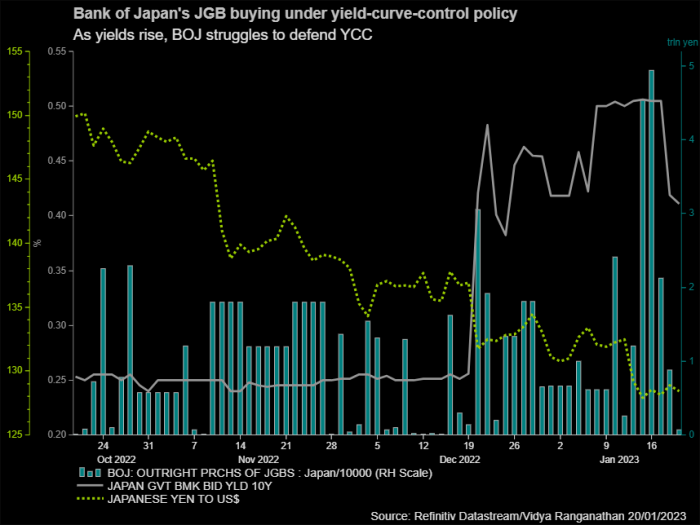

After Wednesday’s decision to retain ultra-low rates, 10-year bond yields, which had been testing the BOJ’s 0.5% cap for a week, settled below 0.4%, suggesting many speculators were closing positions.

And there were falls in interest rate swaps and longer-tenor bonds, which had become the target of the feverish speculation while the BOJ bought billions of yen worth JGBs to keep 10-year yields pegged. The 10-year swap has fallen to 0.75% from above 1% before the meeting.

The cost of the short JGB trade, famously dubbed the ‘widowmaker’ for its penchant to fail, is roughly 6% annualised, making it punitive for short-sellers if the BOJ stays pat for long.

Also, with the BOJ owning more than 50% of outstanding bonds and almost all of the 10-year benchmarks, and its move this week to give banks a lot more cheap money, market participants worry that an already illiquid JGB market will become more so.

‘Risky to sell’

“It is risky to sell now, so in the next month bond prices will be firm,” said Masayuki Koguchi, general manager at the fixed income investment division of Mitsubishi UFJ Kokusai Asset Management.

“In the short term, because of the BOJ’s huge holdings in JGBs, demand and supply balance is tight. I want to see how far yields will fall.”

Concerns over liquidity and the ability to buy JGBs in time were the reasons most other short-sellers covered their short positions this week, bankers said.

Most investors do not expect to hunker down for long, however, and are preparing to return to the trade before April when there is a change of guard at the BOJ after Governor Haruhiko Kuroda and two of his deputies step down.

“Most people are concerned about market liquidity in the bond market,” a senior trader at a global bank in Asia said.

“I think depending on market developments, if liquidity gets worse, people will unwind their positions – not because they are changing their view, but because they are really concerned about the market dislocation.”

Focus shifts to yen

The arena for betting on monetary tightening has in the meantime moved to currency markets, with the yen the target of speculation that rising yields will lift its value, too.

“We think the way to capitalize on it (YCC abandonment) is actually to be long yen, rather than short the government bond, and you get more bang for the buck from doing that,” Jonathan Liang, head of Asia ex-Japan investment specialist for global fixed income, currency and commodities at JPMorgan Asset Management, told a media gathering this week.

The relentless yen buying has seen it rise 18% against the dollar since mid-October and to an 8-month high of 127.215 this week, helped in part by the dollar’s drop from highs as markets priced in less aggressive rate rises by the Fed.

“A lot of macro funds still believe that we could see the 10-year yield between 0.7% to 1% by the end of the year,” said Tareck Horchani, head of dealing for the prime brokerage at Maybank Securities.

But, for that to happen, there would need to be clear signals around policy change from the BOJ, which was unlikely until a new governor takes charge, he said.

“However, the positioning for dollar-yen downside has not changed. I believe actually that it will increase, especially if we see more weak economic data coming out of the US.”

- Reuters with additional editing by Jim Pollard

Also read:

Japan’s Top Economists Debate Dumping ‘Abenomics’

Netherlands to Consult Japan, Taiwan on US-China Chip Curbs

India Passes Japan to Become No-3 Car Market – Nikkei