G20 nations, whose financial heads meet in Venice this week, and policymakers from across the world need to speed up efforts to boost access to vaccinations in poor countries, not only to save lives, but ensure that the world enjoys a smoother economic recovery from the Covid-19 pandemic. A report by IMF head Kristalina Georgieva:

WHEN G-20 finance ministers and central bank governors gather in Venice this week, they can take inspiration from the city’s unbreakable spirit.

As the world’s first international financial centre, Venice has faced the vagaries of economic fortunes over centuries, while being directly affected by climate change. This extraordinary resilience is needed more than ever as policymakers continue to face extraordinary challenges.

The good news is that the global recovery is progressing broadly in line with the IMF’s April projections of 6% growth this year. After a crisis like no other, we are seeing in some countries a recovery like no other, propelled by a combination of strong fiscal and monetary policy support and rapid vaccinations.

For the United States, for example, we project 7% growth this year, the highest since 1984. The recovery is similarly gaining momentum in China, the euro area, and a handful of other advanced and emerging economies. But incoming data also confirm a deepening divergence in economic fortunes, with a large number of countries falling further behind.

The world is facing a worsening two-track recovery, driven by dramatic differences in vaccine availability, infection rates, and the ability to provide policy support. It is a critical moment that calls for urgent action by the G20 and policymakers across the globe.

As our note to the G20 meeting points out, speed is of the essence. We estimate that faster access to vaccinations for high-risk populations could potentially save more than half a million lives in the next six months alone.

Dangers of divergence

Low vaccination rates mean that poorer nations are more exposed to the virus and its variants. While the Delta variant is raising concerns everywhere, including in G20 nations, it is now driving a brutal surge in infections in sub-Saharan Africa. In that region, less than 1 adult in a hundred is fully vaccinated, compared to an average of over 30% in more advanced economies. Unvaccinated populations anywhere raise the risk of even deadlier variants emerging, undermining progress everywhere and inflicting further harm on the global economy.

Shrinking fiscal resources will make it even harder for poorer nations to boost vaccinations and support their economies. This will leave millions of people unprotected and exposed to rising poverty, homelessness, and hunger. The crisis has already caused rising food insecurity, and concerns are now growing in many countries over further spikes in food price inflation.

The world is also keeping a close eye on the recent pickup in inflation, particularly in the US. We know that accelerated recovery in the US will benefit many countries through increased trade; and inflation expectations have been stable so far. Yet there is a risk of a more sustained rise in inflation or inflation expectations, which could potentially require an earlier-than-expected tightening of US monetary policy. Other countries face similar challenges from higher commodity and food prices.

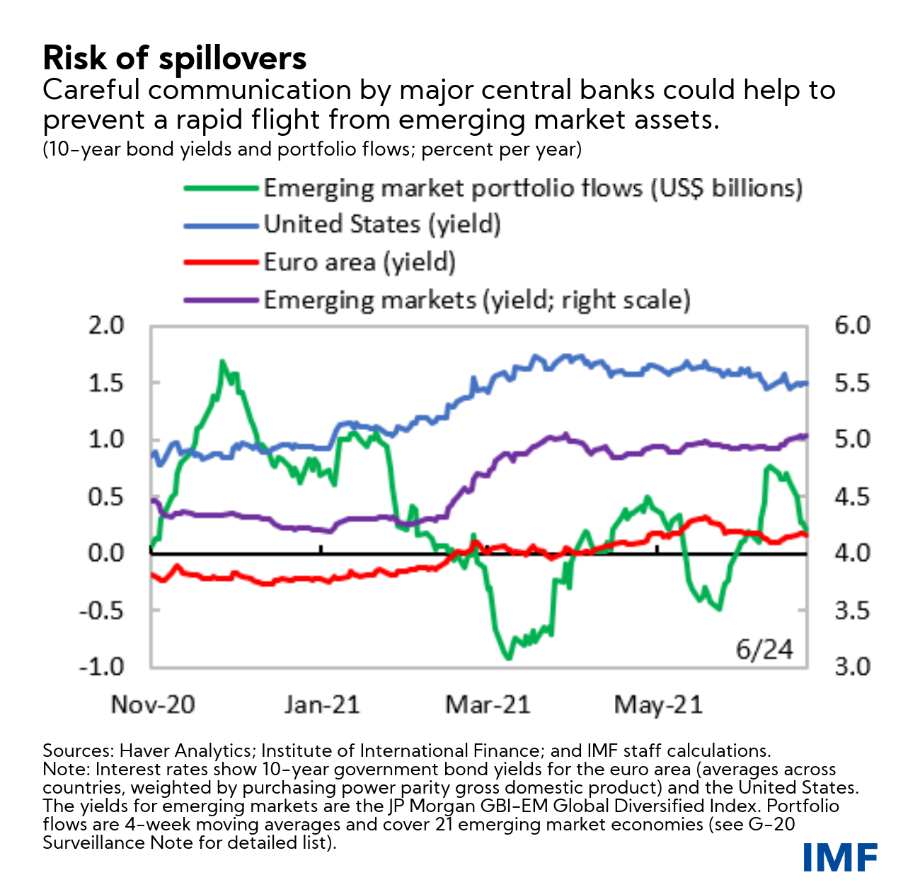

Higher interest rates in the US could lead to a sharp tightening of global financial conditions and significant capital outflows from emerging and developing economies. It would pose major challenges especially to countries with large external financing needs or elevated debt levels.

It bears repeating that this is a critical moment for the world. If we are to address this worsening two-track recovery, we must take urgent policy action now.

First, step up international cooperation to end the pandemic.

The economic benefits would be extraordinary, and potentially saving hundreds of thousands of lives in the next few months is a moral imperative. The costs are relatively small.

IMF staff recently outlined a $50 billion plan that could lead to trillions of dollars gained from faster vaccine rollout and accelerated recovery. This would be the best public investment of our lives and a global game-changer.

To accelerate the implementation of actions outlined in this plan, the IMF, World Bank, WHO, and WTO have formed a ‘war room’. At our first meeting last week, convened by the World Bank, we agreed to work together to help track, coordinate, and advance delivery of vital health tools to developing countries and to mobilize policymakers to remove critical roadblocks.

Support from the G20 and other economies will make all the difference by endorsing the vaccination target of at least 40% of the population in every country by the end of 2021, and at least 60% by the first half of 2022.

To reach these targets, critical actions would include more dose sharing with the developing world; supporting grant and concessional financing to increase and diversify vaccine production, and bolster in-country delivery, diagnostics, and therapeutics; and removing all barriers to exports of inputs and finished vaccines, and other barriers to supply chain operations.

Adapting rapidly to changing circumstances, such as the surge in infections in sub-Saharan Africa, is also essential.

Second, step up efforts to secure the recovery.

Led by G-20 economies, the world has taken extraordinary and synchronized measures, including about $16 trillion in fiscal action. Now is the time to build on these efforts with measures that are tailored to countries’ pandemic exposure and policy space.

In countries where infections are rapidly rising, it is critical that healthcare and vulnerable households and firms continue to receive support. This requires targeted fiscal measures, within credible medium-term frameworks.

Once improvements in health metrics allow for a normalization of activity, governments should gradually scale back support programmes — while scaling up social spending and training programs to cushion the impact on workers. This would help heal the scars of the crisis, which hit young people, women, and the low-skilled especially hard.

Securing the recovery also requires continued monetary accommodation in most countries. This has to be coupled with closely monitoring inflation and financial stability risks. In countries where the recovery is accelerating, including the US, it will be essential to avoid overreacting to transitory increases in inflation.

In order to keep inflation expectations well anchored, major central banks have to carefully communicate their policy plans. This would also help prevent excess financial volatility at home and abroad. The key is to prevent the types of spillovers we saw earlier this year.

Third, step up support to vulnerable economies.

Poorer nations are facing a devastating double-blow: they are at risk of losing the race against the virus; and they could lose the opportunity to join a historic transformation to a new global economy built on green and digital foundations.

We estimate that low-income countries have to deploy some $200 billion over five years just to fight the pandemic. And then another $250 billion to have the fiscal space for transformative reforms, so they can return to the path of catching up to higher income levels. They can cover only a portion of that on their own. It is therefore vital that wealthier nations redouble their efforts, especially on concessional financing and dealing with debt.

The G20 Debt Service Suspension Initiative has provided fiscal breathing space. But given the need to provide permanent debt relief, we must make the new Common Framework fully operational. Chad, for example, received financing assurances from its G20 bilateral creditors, and we now need speedy commitments, on comparable terms, by private creditors.

We also strongly encourage the timely formation of the creditor committee to enable the delivery of the debt operation that Ethiopia is requesting. Success in the first Common Framework cases is critical for other countries with unsustainable debt burdens or protracted financing needs. They should also seek early action for debt resolution or reprofiling.

The IMF’s role

For its part, the IMF has stepped up in an unprecedented manner by providing $114 billion in new financing to 85 countries and debt service relief for our poorest members. We have received support to increase access limits, so we can scale up our zero-interest lending capacity. And we are exploring a new ‘vaccine window’ under our emergency financing facilities, which would support countries in financing vaccination programs if needed.

Our membership also backs a new allocation of Special Drawing Rights of $650 billion, the largest issuance in the IMF’s history. It will supplement reserves and help all our member countries, especially the most vulnerable, address their emergency needs, including vaccines. Our Executive Board recently discussed the proposal, and we expect the allocation process to be completed by the end of August.

In addition, we are working towards magnifying the impact of the new SDR allocation — by encouraging voluntary channeling of some of the SDRs, together with budget loans, to reach a total global ambition of $100 billion for the poorest and most vulnerable countries. We are exploring with our membership ways to get this done, including through our Poverty Reduction and Growth Trust (PRGT) and possibly a new Resilience and Sustainability Trust (RST).

This week’s G20 meeting is an opportunity to advance the plan for a new RST, which would support low-income nations as well as poorer and vulnerable middle-income countries ravaged by the pandemic. It would help them with structural transformation, including confronting climate-related challenges.

To further step up action on climate change, IMF staff recently proposed an international carbon price floor. Such a floor could help accelerate the transition to low-carbon growth over the course of this decade, and we intend to make a strong case for it at this week’s G20 Venice Conference on Climate.

On taxation, we strongly welcome the historic agreement reached by 130 countries in the context of the OECD/G20 Inclusive Framework. Under this accord, a minimum corporate tax rate will help ensure that highly profitable companies pay their fair share everywhere. We know from our own research that minimum tax regimes can help countries preserve their corporate tax base and mobilize revenue. This is now more important than ever.

Decades of tax competition fueled a race to the bottom — thus starving many countries of the resources needed to make vital investments in health, education, infrastructure, and social policies. Fiscal policies came under further strain during the pandemic, which makes it more difficult to invest in green and digital transformations. So, let’s seize this crucial moment to build a fairer and more effective international tax system that is fit for the 21st century.

We can end the pandemic and turn this two-track recovery into synchronized and sustainable growth — by acting decisively and acting together.

Kristalina Georgieva is Managing Director of the IMF.

Her full report is here.