For global banks and fund managers drawing up their 2022 China investment strategies, one factor occupies their minds but eludes valuation models: President Xi Jinping’s next five years in office.

Having done away with term limits in 2018, China’s most powerful leader since Mao Zedong is steering the country back towards its socialist roots, upending financial markets.

Crackdowns on internet giants, property developers and education have MSCI’s China index down 20% in 2021 against a 15% rise in world stocks, while China’s once-popular high-yield debt market has crumbled.

There is a growing consensus that the selling is overdone, but with Xi all but assured an unprecedented third term next year and with policy in flux, investors have said positioning for the era to come is a more delicate task than simply bargain hunting.

“What you buy today and what you buy in the future will be quite different from what you bought last year, five years ago or 10 years ago,” Chi Lo, senior strategist at BNP Paribas Asset Management in Hong Kong, said.

New Xi Regime

“The new regime under the Xi Jinping government is going to be more properly supervised, more regulated,” he said.

“Companies’ operation models will have to change… what the Chinese government wants to develop will be the key to decide your portfolio’s composition.”

Lo suggested avoiding “sunset” sectors such as coal and steel to focus on apparent priorities such as high-tech manufacturing or emissions reduction projects.

Other global banks have offered similar ideas.

Goldman Sachs compiled a 50-stock “common prosperity portfolio” containing renewable energy firms, some consumer-exposed companies, plus tech and state-owned firms with a focus on research, among others.

‘New Heroes’ in China

JP Morgan has highlighted the potential of “new heroes” in electric vehicles, such as BYD, and advanced manufacturing, while “old heroes” in the property sector fade.

Jack Siu, chief investment officer for Greater China at Credit Suisse, is on watch for a possible upgrade in company earnings next year, as “we will likely see some supportive fiscal policy and moderately or slightly less tight monetary policy” ahead of the party’s next Congress, which could usher in another term for Xi.

Morgan Stanley expects an above consensus economic recovery to 5.5% growth in 2022 as policy is eased.

Société Générale (SocGen), which says China has the highest potential for upside in Asia next year, is overweight on staples, 5G and high-end manufacturers. It said China’s blue-chip CSI300 aligns better with policy priorities than MSCI’s index, which has heavy weightings to some out-of-favour internet firms.

“While we believe that risk/reward has improved for internet names, we maintain a strategy of gaining exposure to common prosperity themes, on a structural policy tailwind,” SocGén strategists said in their Asia outlook note.

Common Good

“Common prosperity” isn’t a new concept in China, having first been mentioned by Mao in the 1950s. It has gained currency as a Xi-era catchphrase for a new drive to narrow a yawning wealth gap and foster more inclusive growth.

Xi has also renewed efforts to deleverage the property sector, sought to curtail tech firms’ grip on data and commerce, and promised carbon neutrality by 2060.

What has hit markets and put investors on guard is less the programme’s broad direction – which bulls say now seems set for the next decade or so – than its unpredictable application, especially as Xi consolidates power.

To be sure, policy risk is ever-present in China. But a year of seismic shifts – sometimes heralded via gnomic regulatory comments in state media or a confusing melange of leaks – makes it front of mind.

“That’s a large worry for us, because you don’t really know what the Chinese Communist Party’s thinking,” Mark Arnold, chief investment officer at Hyperion Asset Management in Brisbane, said.

One-Party State to One-Person State

“You’ve really got an all-powerful government, a one-party state really developing into a one-person state, so you don’t have the feedback loops or protections of democracy.”

Still, flows suggest it is not yet scaring foreigners away from stocks, according to data from BNY Mellon, which shows consistent equity flows this year against selling in bonds that have been hurt by a crackdown on developers’ borrowing.

Foreign inflows into China’s stock market totalled 241 billion yuan ($40 billion) for the year to the end of September.

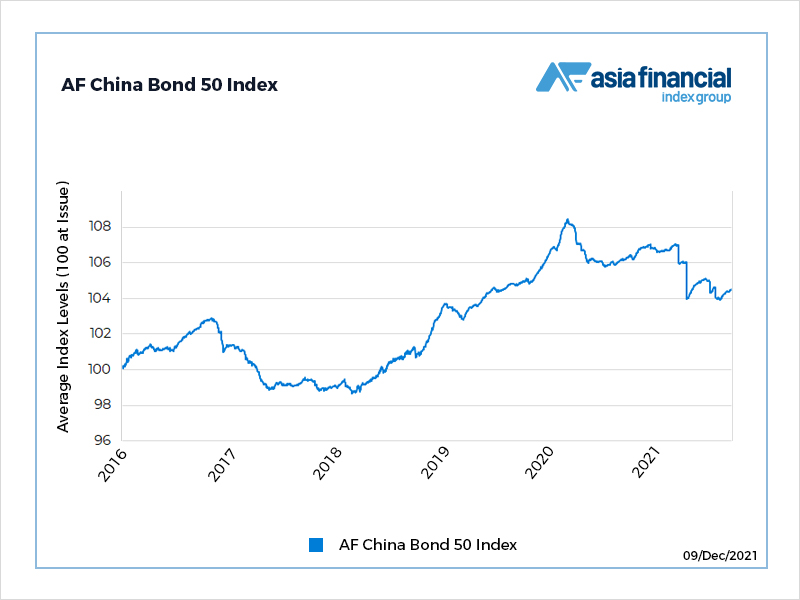

Inflows into China’s interbank bond market totalled 598 billion yuan in the first 10 months of 2021, up 18.4% from the end of 2020. An ICE BofA index of Chinese investment grade bonds has been steady this year against a 30% plunge in the Chinese high-yield index.

For some, the risk of missing out on China looms larger than the danger of getting hurt.

“If you’re a global pension fund and all your eggs are in the US basket, and you’ve got nothing in China, it’s quite a skewed portfolio,” Jim McCafferty, joint head of equity research in Asia at Nomura in Hong Kong, said.

“As soon as we see US equities start to underperform and Chinese equities, which of course are cheap on all valuation benchmarks, start to outperform – that’s the point in time where I think investors will start agitating.”

- Reuters

ALSO SEE:

Xi Jinping outlines plans for many years ahead

Xi Vows to Address Trade Concerns: SCMP

Xi Scaling Back National Property Tax Plan: WSJ